If you have been involved in a car accident, your Uninsured or Underinsured Motorist (UI/UIM) insurance may be the best investment you have ever made! Why? In the USA, ~14 % of drivers are uninsured (~32–35 million) as of 2022, not to mention the tens of millions more that drive with only state-mandated minimum coverages.

If you have been involved in a car accident, your Uninsured or Underinsured Motorist (UI/UIM) insurance may be the best investment you have ever made! Why? In the USA, ~14 % of drivers are uninsured (~32–35 million) as of 2022, not to mention the tens of millions more that drive with only state-mandated minimum coverages.

To protect yourself and your family against at-fault drivers who have little-to-no auto insurance coverage, it is imperative you purchase UI/UIM insurance. The goal of this blog is to review exactly what UI/UIM insurance is, why it is important, and the average cost of adding this type of insurance to a policy. I will also be letting you in on little secret insurance companies don’t want you to know: their #1 determining factor used to set your insurance premiums. Hint: it is NOT just your driving record.

Bridging The Gap

In Oregon, it is estimated that 14-16% of drivers operate with NO insurance coverage in spite of the legal requirement to maintain insurance coverage at all times. While that is disturbing, it is equally alarming that an even larger percentage of Oregon drivers have only the Oregon mandated minimum coverage.

This minimum insurance coverage is adequate for minor accidents, but if you have been involved in a major automobile accident, then the at-fault driver with the minimum coverage may not be able to adequately compensate you for your injuries and financial losses. Think about it… almost 40% of Oregon car accidents involve bodily injuries with a significant number of accidents involving moderate to serious injuries and typical recuperation costs of $150,000 to $500,000. This does not address the cost of catastrophic accidents, such as a traumatic brain injury or spinal cord injury, where the insurance proceeds may need to support a lifetime of medical treatment, lost wages, and pain and suffering, and can easily top $2-5 million.

This is where YOUR Uninsured or Under-Insured Motorist (UI/UIM) coverage can provide the financial resources to bridge the gap between the minimal insurance coverage of the at-fault driver and what you really need to compensate you for all of your financial, physical, mental and emotional losses.

What is UM/UIM insurance?

Uninsured Motorist Coverage

Every driver operating a vehicle in Oregon is required, by law, to have at least the mandated minimum insurance coverage. Unfortunately, not all drivers carry current insurance. This is where your Uninsured Motorist coverage benefits you. If you are injured through the fault of an uninsured driver, or a hit-and-run driver, then your Uninsured Motorist policy will provide coverage up to the limits of your policy.

Simply put, your insurance company steps in and covers your damages when the other driver has NO insurance.

If you have the minimum coverage, then you will be covered for $25,000 in damages per person and $50,000 per accident if multiple people in your car are hurt. However, if you increase the UM/UIM coverage limits on your auto policy to the recommended $250K to $500K or more, you significantly improve your chances of covering your damages in the event of a bad car accident.

An Example: A client of mine was injured when she was hit by an uninsured driver. She incurred nearly $50,000 in medical bills and $20,000 in lost wages. Fortunately, she had UM insurance of $250,000, which covered all of her financial losses and provided compensation for her pain and suffering.

Underinsured Motorist Coverage

In the event you are involved in an accident where the at-fault driver does not have sufficient insurance coverage to pay for your damages, then you may be entitled to additional compensation if your UIM coverage limits are greater than the at-fault driver’s insurance limit.

For example, if you have $500K in UM/UIM coverage (per accident) and the at-fault driver has only the mandated minimum, then you would have an additional $475K in insurance coverage through your policy to compensate you for your damages. As of 2016, Oregon allows “stacking” of Uninsured and Underinsured Motorist (UM/UIM) coverage for policyholders, meaning coverage limits from multiple vehicles or policies can be combined.

Under the Oregon law effective Jan 1, 2016, now UIM benefits can stack: all new motor vehicle liability policies issued in Oregon will include UM/UIM insurance coverage that can be added to the bodily injury coverage for at-fault drivers. For instance, let’s say both drivers have the state-mandated minimum insurance coverage of $25,000 per person and the driver who is not at-fault has injuries and damages in excess of $25,000. The injured victim can stack her UIM coverage of $25,000 on top of the at-fault driver’s bodily injury coverage of $25,000 for $50,000 in total insurance coverage.

What does UM/UIM insurance cost?

You might not be aware that UM/UIM rates above the mandated minimum can be very affordable. Recent quotes for $500K UM/UIM insurance limits ranged from $40 to $95 per year. You can also add $1,000,000 excess UM/UIM coverage to an umbrella policy for an additional $50-$175 per year. Of course, rates are influenced by many factors, some of which are discussed below. I suggest getting insurance quotes from multiple insurance companies to compare policies and prices. — For the purposes of this blog, I obtained 180 quotes on car insurance.

Why are so many Oregon drivers driving without insurance or with only the minimum coverage?

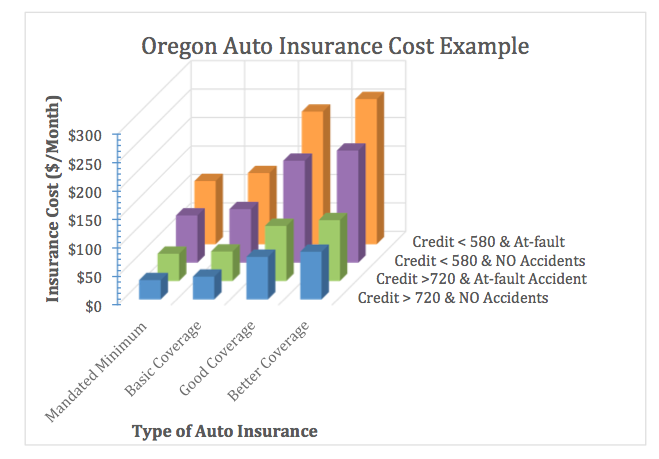

You would think that Oregon insurance companies set rates based upon an individual’s driving record, and you would be correct, but the most significant factor affecting your premium is your credit information.

Simply stated, two individuals with the same driving history, policy types, coverage limits, vehicles, and zip codes, but with different credit scores will have substantially different insurance costs. Insurance premiums for policies where the insured has “Poor Credit” can be more than 200% HIGHER than a similar individual with “Excellent Credit.”

Simply stated, two individuals with the same driving history, policy types, coverage limits, vehicles, and zip codes, but with different credit scores will have substantially different insurance costs. Insurance premiums for policies where the insured has “Poor Credit” can be more than 200% HIGHER than a similar individual with “Excellent Credit.”

If that wasn’t bad enough, a driver with poor credit and a great driving record will still pay between 170% and 220% MORE than a driver with excellent credit and an extremely bad driving record (DUI/DWI and/or an at-fault accident with bodily injury and property damage)!

Insurance companies believe your credit rating is a better predictor of your future accident potential than your driving record.

This practice often penalizes people who can least afford higher insurance costs. A few states, including California, Hawaii, and Massachusetts, prohibit using credit scores in setting auto insurance premiums, relying instead on factors like driving record, vehicle type, mileage, and safety features—which can lower costs for many families.

Bottom-line: It is worth the investment to protect your family from other drivers who have no insurance or minimal insurance by obtaining adequate UM/UIM insurance coverage.

Portland Personal Injury Attorney

As a Portland personal injury attorney, my sole focus is to represent victims and their families who have been wrongfully injured as a result of another’s careless or intentional conduct. I hope this website is a place to learn more about our law firm, as well as, an educational resource for Oregonians who have been victims of accidents. It is not intended to be legal advice, as every case is unique and should be accurately evaluated.

As a Portland personal injury attorney, my sole focus is to represent victims and their families who have been wrongfully injured as a result of another’s careless or intentional conduct. I hope this website is a place to learn more about our law firm, as well as, an educational resource for Oregonians who have been victims of accidents. It is not intended to be legal advice, as every case is unique and should be accurately evaluated.

If you or someone you know has been injured as a result of another person’s conduct, and you are looking for a skilled attorney to lead you through the insurance roadblocks, please call today for a free and confidential case evaluation. Local (503) 444-2825 Toll-free 1 (800) 949-1481 or email travis@mayorlaw.com.

For additional information about personal injury cases, insurance, and maximizing your financial recovery, I recommend the following articles on my Blog:

Travis Mayor Named Rising Star by Oregon Super Lawyers

8 Mistakes Insurance Companies Are Hoping You Make!

Oregon Car Accident Guide: Protect Your Rights and Maximize Your Financial Recovery

Oregon Car Insurance and Personal Injury Claims FAQs